You have to pay provisional tax in New Zealand if your untaxed income results in a residual tax bill of more than $5,000 at the end of the financial year, meaning you must pay your income tax in regular instalments rather than a single lump sum.

When you work a traditional job as a PAYE (Pay As You Earn) employee in New Zealand, tax is virtually invisible. It slides quietly out of your paycheck every fortnight before the cash ever hits your bank account, taking care of your income tax, ACC levies, and KiwiSaver contributions automatically. But the moment you strike out on your own as an independent contractor, freelance designer, or self-employed sole trader, that protective bubble bursts. Suddenly, you are receiving 100% of your gross invoice amounts. While seeing those unclipped sums drop into your business account feels amazing, it comes with a massive catch: a large portion of that cash does not belong to you.

Many new Kiwi business owners in Auckland, Wellington, and Christchurch get caught out during their second year of trading because they do not prepare for the shift in tax timing that occurs when you are self-employed. Known commonly as the “first-year tax trap,” this phenomenon blindsides thousands of contractors every year, leaving them with unexpected debt and a massive scramble to find money for the Inland Revenue Department (IRD). This comprehensive, up-to-date guide for the 2026/2027 tax year will break down exactly how provisional tax works, help you determine if you need to pay it, compare the calculation methods available to you, and lay out a clear framework to keep your cash flow perfectly protected.

What Is Provisional Tax and Why Does It Exist?

The most important thing to understand is that provisional tax is not an additional or separate type of tax. It is simply a method of paying your regular income tax in pre-determined instalments throughout the financial year, rather than waiting to settle the entire bill at the end. The IRD uses this system to keep cash flowing into the government’s coffers steadily, bringing self-employed earners into closer alignment with how PAYE employees pay their tax step-by-step.

The reason it causes so much stress is the structural lag in New Zealand’s tax calendar. When you first begin contracting or running a sole trader business, you generally do not pay any tax during your first twelve months. You collect your income, pay your business expenses, and wait until the end of the standard financial year (31 March) to file your individual tax return (IR3).

The financial shock arrives in your second year. Once you file that first tax return, the IRD will issue you a bill for your first year’s earnings, known as terminal tax. However, because they now know your business is consistently profitable, they will also require you to start paying provisional tax instalments for your second year at the exact same time. This creates a “double tax year” effect where you are paying off last year’s tax while simultaneously pre-paying the current year’s tax. If you haven’t budgeted for this accumulation, it can completely cripple a young business’s working capital.

The $5,000 Residual Income Tax (RIT) Threshold

Whether or not you have to step onto the provisional tax treadmill depends entirely on a metric called Residual Income Tax (RIT). In plain English, your RIT is your total individual income tax liability for the financial year minus any tax that has already been deducted at source (such as PAYE from a part-time job, schedular payments deducted by a recruiter, or Resident Withholding Tax on your bank interest accounts).

For the 2026 and 2027 tax years, the entry threshold stands firmly at $5,000 of RIT.

- If your RIT is $5,000 or less: You are exempt from provisional tax rules. You simply file your annual IR3 return and pay your full tax bill as a single terminal tax lump sum the following year.

- If your RIT is more than $5,000: You automatically enter the provisional tax system for the next financial year. The IRD will notify you of your obligation and assign you payment dates.

The Three Provisional Tax Methods Compared

To offer flexibility for different styles of business, the IRD allows you to choose from three core methods to calculate and pay your interim tax. Selecting the right path can be the difference between smooth financial sailing and severe cash constraints.

1. The Standard (Uplift) Method

This is the automatic, default option used by the overwhelming majority of Kiwi sole traders and contractors. It looks backward to find safety. The IRD takes the RIT from your most recently filed tax return and adds a 5% uplift to it, operating on the assumption that your business will grow slightly year-on-year.

If you have not filed your previous year’s tax return yet when an instalment falls due, the IRD looks back two years and applies a 10% uplift instead. The major advantage of the standard method is its “safe harbour” feature: if your income unexpectedly skyrockets during the year, you are protected from interest penalties as long as you pay your uplifted amounts on time.

2. The Estimation Method

If you know with absolute certainty that your business is going to make significantly less money this year than last year — perhaps because you are taking parental leave, downscaling your client list, or dealing with a major market downturn — you can actively choose to estimate your tax.

You calculate what you expect your current year’s RIT to be, and the IRD divides that number across your payment dates. The massive risk here is precision. If you underestimate your earnings and end up paying less than your actual year-end tax liability dictates, the IRD will charge you backdated interest on the shortfall.

3. The AIM (Accounting Income Method)

AIM is a modern, software-driven “pay-as-you-go” system designed specifically for small businesses and contractors with an annual gross turnover under $5 million. Instead of predicting the future or relying on ancient history, AIM connects directly into cloud accounting platforms like Xero or MYOB.

Your software automatically calculates your exact tax liability at the end of every month or two-month cycle based on your real, actual profits. If you have a terrible month with zero profit, your tax liability for that period is $0. If you have a massive trading month, you pay more. It largely eliminates year-end surprises and interest exposure.

| Feature / Metric | Standard (Uplift) Method | Estimation Method | AIM (Accounting Income Method) |

|---|---|---|---|

| How it is Calculated | Previous year’s RIT + 5% uplift | Your own forecast of current year profit | Real-time calculations via software |

| Best Suited For | Stable, predictable, or growing businesses | Declining businesses or those closing down | Highly seasonal or volatile incomes |

| Interest Risk (UOMI) | Extremely low (protected by Safe Harbour) | High risk if you underestimate your income | No interest risk if software settings match |

| Payment Frequency | 3 instalments per year (for standard filers) | 3 instalments per year (for standard filers) | Matches your GST filing dates (monthly/2-monthly) |

2026/2027 Provisional Tax Instalment Dates

For the vast majority of Kiwi self-employed individuals running on the standard 31 March financial balance date, your provisional tax is broken into three equal chunks across the year. If a due date lands on a weekend or a public holiday, the deadline naturally rolls over to the next official working business day.

The standard layout for the 2026/2027 tax cycle is structured as follows:

| Instalment | Due Date (Standard 31 March Balance) | Payment Breakdown |

|---|---|---|

| Instalment 1 (P1) | 28 August 2026 | 1/3 of your total provisional tax liability |

| Instalment 2 (P2) | 15 January 2027 | 1/3 of your total provisional tax liability |

| Instalment 3 (P3) | 7 May 2027 | Final 1/3 of your total provisional tax liability |

| Terminal Tax | 7 February 2028 (or 7 April 2028 if you use a tax agent with an extension of time) | The final square-up balance after your actual return is filed |

Important variation: If you are registered for GST and choose to file your GST returns on a 6-monthly basis, your provisional tax instalments drop from three payments down to two. These align with your GST deadlines and fall on 28 October and 7 May each year.

How to Calculate Under the Standard Method: A Real Example

Let’s look at how the math actually applies to a real-life Kiwi sole trader using the standard uplift pathway.

Meet Liam, a freelance construction contractor based in Christchurch. For the financial year ending 31 March 2025, Liam’s total self-employed profit left him with a final Residual Income Tax (RIT) bill of $18,000. Because this comfortably clears the $5,000 threshold, Liam is required to pay provisional tax for the 2025/2026 tax year.

Here is how his calculations play out step-by-step:

- Calculate the 5% uplift: The IRD takes his 2025 RIT and adds the mandatory 5% buffer.

$18,000 × 1.05 = $18,900 total 2025/2026 provisional tax liability - Divide into the standard dates: Because Liam files GST on a standard 2-monthly basis, his total is split into three equal parts.

$18,900 ÷ 3 = $6,300 per instalment

Liam pays $6,300 on 28 August 2025, $6,300 on 15 January 2026, and $6,300 on 7 May 2026.

When the 2026 financial year concludes, Liam’s business has boomed, and his actual real tax liability for the year finishes at $22,000. Because Liam used the standard uplift method and paid every single instalment on time, he faces no interest penalties for the difference. He simply pays the remaining balance of $3,100 ($22,000 actual tax minus the $18,900 already paid) as terminal tax on 7 February 2027 — or 7 April 2027 if he’s registered with a tax agent who holds an extension of time.

The Consequences of Underpaying: UOMI & Penalties Explained

Failing to meet your provisional tax due dates triggers an aggressive response from the IRD’s automated systems. If you miss a deadline, late payment penalties hit you immediately:

- A 1% penalty is added to the outstanding balance the very day after the payment was due.

- An additional 4% penalty is applied to the debt seven days later if it remains unpaid.

In addition to these static penalties, the IRD charges a daily variable interest rate called Use-of-Money Interest (UOMI). The IRD treats any underpaid tax as a line of credit you have taken out from the New Zealand government. These rates are reviewed periodically by IRD, so it’s worth confirming the current figures on IRD’s website before relying on them — as of early/mid-2026 they sit at:

- The Underpayment (Debit) Rate: The IRD charges 8.97% per annum on any underpaid tax balances, calculated daily from the day after the due date until the principal is cleared.

- The Overpayment (Credit) Rate: If you overpay your tax, the IRD does pay you interest, but only at a rate of 2.25% per annum.

The $60,000 Safe Harbour Rule: If your actual RIT for the current year is less than $60,000, and you have calculated and paid all your provisional tax instalments on time using the standard uplift method, you are deemed a “Safe Harbour” taxpayer. This means the IRD will not charge UOMI on any shortfall for your instalment dates during the year. Interest will only start ticking if your final wash-up bill isn’t settled by your terminal tax date the following year. However, if your RIT exceeds $60,000, safe harbour protection dissolves, and UOMI can be backdated to earlier instalments.

Managing Cash Flow: The 30% Savings Account Rule

To prevent provisional tax from ever keeping you awake at night, you need to implement a strict, non-negotiable cash flow management routine inside your business banking.

- Establish a dedicated tax account (immediate action): Open a completely separate, high-interest business savings account with your bank that is entirely divorced from your everyday business operating account. Label it clearly as ‘Tax Reserves’ so you are never tempted to touch it for general overheads.

- Enforce the 30% rule on every single payment (ongoing discipline): Every time a client pays an invoice, immediately calculate 30% of the gross cash that landed in your account and transfer it straight into your dedicated tax account. If an invoice is for $1,000, $300 moves instantly to the tax account before you pay yourself or clear any expenses.

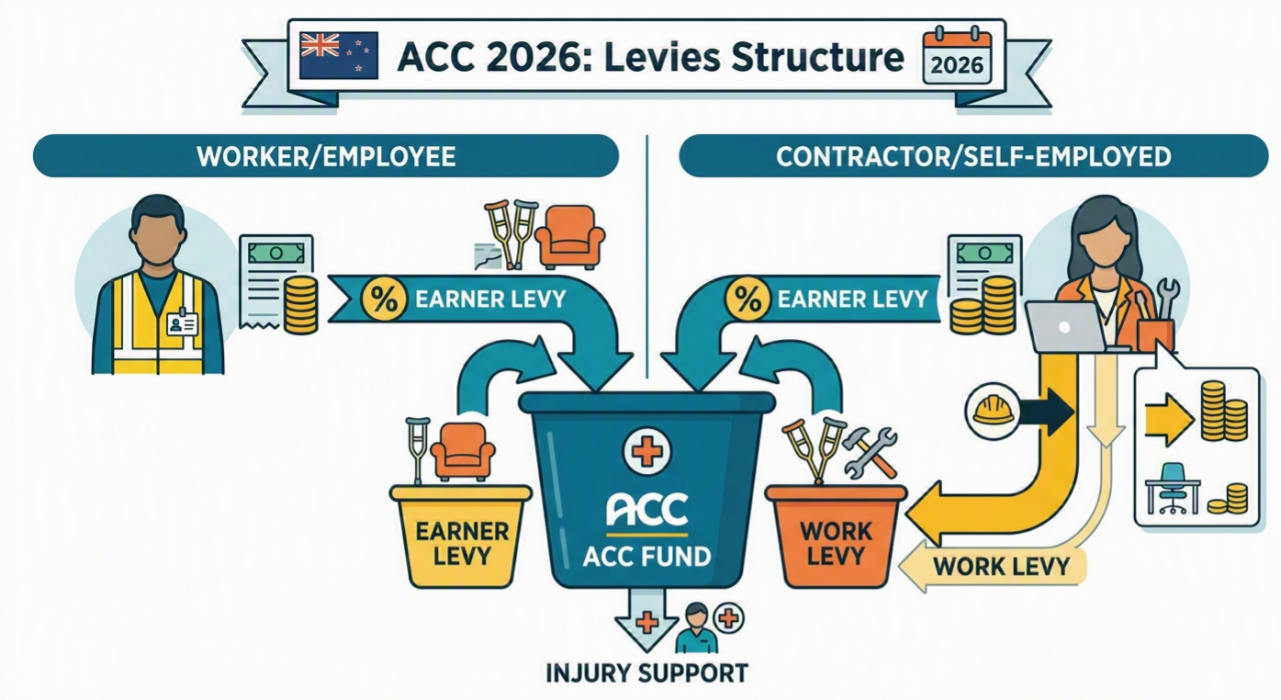

- Factor in ACC levies and KiwiSaver additions (monthly balance check): Remember that your 30% savings bracket isn’t just protecting you from income tax. It also needs to cover your annual ACC bill. As a self-employed person you’ll typically pay the ACC Earners’ levy (around 1.75% of your liable earnings for 2026/27) plus a Work levy that varies depending on your industry classification, plus a small Working Safer levy — so your total ACC bill is usually higher than the earners’ levy figure alone. Budgeting a bit extra here, along with room for any personal KiwiSaver lump-sum deposits to capture the government member contribution, will keep this line item from catching you out.

Tax Pooling: The Legal Safety Net for Kiwi Contractors

If you hit a cash flow bottleneck — perhaps a major commercial client defaults on their payment terms or goes under, leaving you unable to make an upcoming provisional tax instalment — do not despair, and do not simply leave it to accumulate penalties with the IRD. New Zealand law provides a highly efficient system called tax pooling.

Authorised intermediaries like Tax Management New Zealand (TMNZ) and Tax Traders operate large, government-regulated pools of tax credits. If you miss an instalment date or discover at the end of the year that you have underpaid significantly, you can buy tax credits from these pools retrospectively.

Because you are effectively “purchasing” tax that another company paid to the IRD on time back on that specific date, the IRD recognises the payment as met chronologically. This allows you to wipe out late payment penalties and lower your interest costs compared to standard IRD UOMI rates. It provides a vital commercial pressure valve for contractors who experience volatile cash cycles.

Frequently Asked Questions

Do I have to pay provisional tax in my very first year of self-employment?

No, in the vast majority of cases, you do not pay provisional tax during your first year because you do not have a filed historical tax return that shows a residual income tax liability over $5,000. However, do not mistake this for a tax holiday. You are still actively accumulating an income tax liability on every dollar you earn; it simply won’t be collected until your terminal tax date arrives in your second year of trading.

Can a sole trader use the AIM method?

Yes, absolutely. Any independent contractor, sole trader, or freelancer can use the Accounting Income Method (AIM) provided their gross annual business income stays below $5 million. To do this, you must use an approved cloud accounting software system (like Xero or MYOB) that is actively set up to submit your real-time financial profiles directly to the IRD.

What happens if I use the Estimation method and my business revenue drops even further?

If you choose the estimation method and notice halfway through the year that your income has dropped significantly below your original guess, you can submit a revised, lower estimate to the IRD through your myIR account at any point before an instalment deadline. The IRD will recalibrate your remaining payments downwards, ensuring you don’t over-drain your active operational cash.

Is Use-of-Money Interest (UOMI) tax-deductible?

Yes. If you are charged UOMI by the IRD on an underpayment of business income tax, that interest expense is generally tax-deductible against your business income in the financial year it is incurred. Conversely, if you receive UOMI credit interest from the IRD due to overpaying your tax, that interest is considered taxable income and must be declared on your annual return.

Protect Your Business Cash Flow from the Tax Shock

Provisional tax shouldn’t be a source of constant dread or a mathematical mystery. By identifying your exact RIT limits early, choosing a payment method that complements your income frequency, and strictly allocating around 30% of every dollar that clients pay you into an untouchable tax account, you can keep the IRD completely satisfied while keeping your sole trader operation highly liquid and safe.

Are you interested in seeing exactly how your financial take-home position shifts compared to fixed corporate structures? Head over to our Contractor vs Employee Calculator to model your structural tax brackets, analyse your potential write-offs, and map out your optimised path forward.

Disclaimer: This is general information, not personalized financial advice. This article provides general information and educational content only. We are not registered financial advisers. Always speak to a licensed financial advice provider.